Home

Measuring Credit Risk (FRM Part 1 2023 – Book 4 – Chapter 6)

AnalystPrep

Premiered Jul 24, 2024

939 views

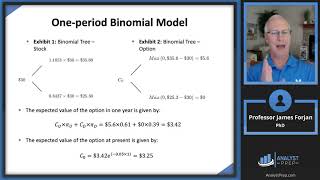

Binomial Trees (FRM Part 1 2023 – Book 4 – Chapter 14)

Correlation Basics: Definitions, Applications, and Terminology (FRM Part 2 – Book 1 – Chapter 7)

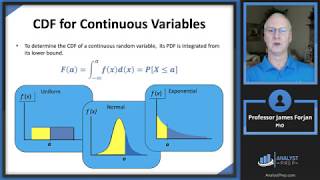

Random Variables (FRM Part 1 2023 – Book 2 – Chapter 2)

Portfolio Risk and Return - Part I (2024/2025 Level I CFA® Exam – PM – Module 1)

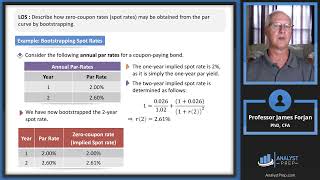

The Term Structure and Interest Rate Dynamics (2024 Level II CFA® Exam –Fixed Income–Module 1)

ALM 101 Webinar

Mad Money - 09/20/24 | Audio Only

Uses of Capital (2022 CFA® Level I Reading 28 – Corporate Issuers)

Common Univariate Random Variables (FRM Part 1 2023 – Book 2 – Chapter 3)

Fundstrat's Tom Lee: Fed cuts set up strong markets next few months but election uncertainty remains

Evolution of Portfolio Theory – From Efficient Frontier to CAL to SML (For CFA® and FRM® Exams)

Why Biden says the US economy has 'entered a new phase': White House's Bernstein

Big Data Projects (2024 Level II CFA® Exam –Quantitative Methods–Module 7)

Beta and CAPM (Calculations for CFA® and FRM® Exams)

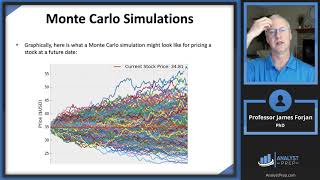

Simulation Methods (FRM Part 1 2023 – Book 2 – Chapter 16)

Interest Rate Swaps Explained | Example Calculation

Normal and Lognormal Distributions (SOA Exam P – Probability – Univariate Random Variables)

You want to own companies that are doing badly and need a rate cut, says Jim Cramer

Value at Risk Explained in 5 Minutes

Times-series Analysis (2021 Level II CFA® Exam – Reading 6)