Home

Trading stock volatility with the Ornstein-Uhlenbeck process

QuantPy

Premiered Mar 7, 2022

26,482 views

The Magic Formula for Trading Options Risk Free

Stochastic Calculus for Quants | Understanding Geometric Brownian Motion using Itô Calculus

Simulating the Heston Model with Python | Stochastic Volatility Modelling

Understanding Market Makers || Optiver Realized Volatility Kaggle Challenge

Historical vs Implied Volatility with 10yrs Options Data!

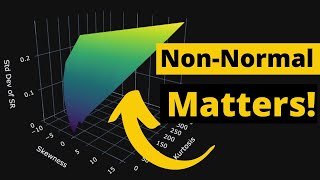

Is your Sharpe Ratio is Lying to you? Use this instead

Stochastic Volatility Models used in Quantitative Finance

Heston Model Calibration in the "Real" World with Python - S&P500 Index Options

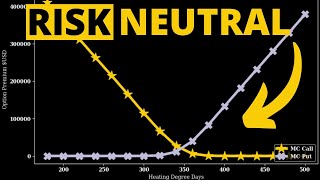

Risk Neutral Pricing of Weather Derivatives

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

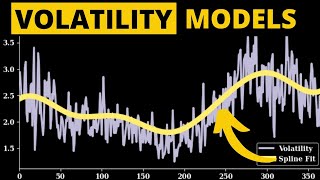

Time Varying Volatility Models for Stochastic Finance | Weather Derivatives

Monte Carlo Simulation of Temperature for Weather Derivative Pricing

Brownian Motion for Financial Mathematics | Brownian Motion for Quants | Stochastic Calculus

Detrending and deseasonalizing data with fourier series

Statistical Analysis of Temperature Data | Time Series Analysis in Python | Weather Derivatives

Stop making investment decisions using this metric!

From Black Holes to Black-Scholes

What is Delta Hedging || Dynamic Delta Hedging like a Quant || Profit & Loss Options Trading

OpenAI & Python: The Ultimate Twitter Automation Guide

Does Index Fund Investing Still Work in 2023?