Home

FRM: Intro to Quant Finance: Volatility

Bionic Turtle

20 ธ.ค. 2007

การดู 54,360 ครั้ง

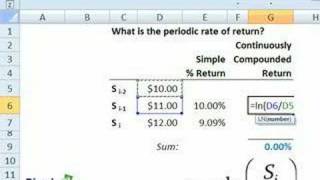

Intro to Quant Finance: Periodic Rate of Return

1. Introduction, Financial Terms and Concepts

Lognormal value at risk (VaR, FRM T5-01)

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

Expected shortfall (ES, FRM T5-02)

Value at Risk (VaR) Backtest (FRM T5-04)

Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

Risk-neutral probabilities (FRM T5-07)

Level 1 Chartered Financial Analyst (CFA ®): Sampling and Estimation

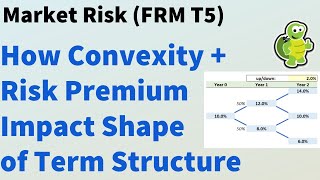

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

External Credit Ratings (FRM T4-44)

Why par yields are the best interest rate measure

Level 1 Chartered Financial Analyst (CFA ®): Common Probability Distributions

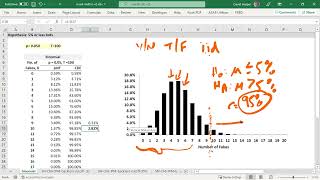

Binomial test: if Elon Musk samples 100 twitter accounts, how many bots (fakes) are too many?

Fixed Income: Key rate shift technique (FRM T4-43)

R Programming: Introduction: ggplot for capital market line (CML, R Intro-08)

CFA - Tackling Classic Duration Questions

R Programming Finance: Load historical stock price series (rfinance-01)

Rank Correlations: Spearman's and Kendall's Tau (FRM T5-06)

A conversation with Mark Meldrum, aka the GOAT (who has joined us at CeriFi by the way)