Home

Bond Duration and Bond Convexity Explained

Ryan O'Connell, CFA, FRM

6 มี.ค. 2022

การดู 95,173 ครั้ง

Calculating Macauley, Modified, and Effective Bond Durations in Excel

Bond Duration Explained Simply In 5 Minutes

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

How The Yield Curve Predicted Every Recession For The Past 50 Years

Fixed Income Markets Explained┃Negative-Yielding Bonds, Duration & Yield Curves

1. Introduction for 15.S12 Blockchain and Money, Fall 2018

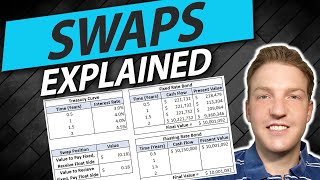

FRM: You will never be scared of SWAPS after watching this!

What is Yield to Maturity? | How to Calculate YTM? | CA Rachana Ranade

Why Bond Yields Are a Key Economic Barometer | WSJ

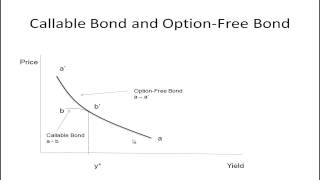

Convexity

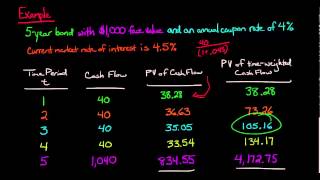

Macaulay Duration

Yield-Based Bond Convexity and Portfolio Properties (2024 CFA® Level I Exam – Fixed Income – LM 12)

Bond convexity

Relationship between bond prices and interest rates | Finance & Capital Markets | Khan Academy

CFA level I: Fixed Income - Super Simplyfied Modified Duration Explained

Interest Rate Swaps Explained | Example Calculation

Killik Explains: Duration - The word every bond investor should understand

สอนพื้นฐาน Excel ตั้งแต่เริ่มต้น แบบครบจบในคลิปเดียว!!

Introduction to the yield curve | Stocks and bonds | Finance & Capital Markets | Khan Academy

Riding the Yield Curve and Rolling Down the Yield Curve Explained