Home

Expected shortfall (ES, FRM T5-02)

Bionic Turtle

18 ก.ย. 2019

การดู 24,405 ครั้ง

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

Three approaches to value at risk (VaR) and volatility (FRM T4-1)

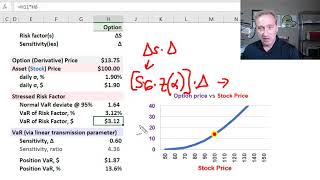

Delta-normal value at risk (VaR, FRM T4-3)

Expected Shortfall & Conditional Value at Risk (CVaR) Explained

Backtesting Expected Shortfall: Generalised breach indicator (GBI)

Love Song 2019_ALL TIME GREAT LOVE SONGS Romantic WESTlife Shayne WArd Backstreet BOYs MLTr

Understanding Basic concept of Value at Risk (VaR) - Simplified

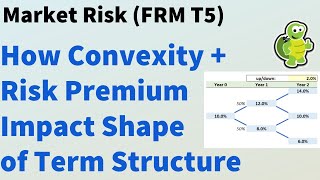

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

Monte Carlo Method: Value at Risk (VaR) In Excel

What is value at risk (VaR)? FRM T1-02

Value at Risk in Excel Historical vs Monte Carlo Methods

Rank Correlations: Spearman's and Kendall's Tau (FRM T5-06)

2015 - FRM : VAR Methods Part I (of 2)

R Programming Finance: Load historical stock price series (rfinance-01)

VaR (Value at Risk) and CVaR (Conditional Value at Risk) Explained in Graphics

FRM: Lognormal value at risk (VaR)

Fixed Income: Key rate shift technique (FRM T4-43)

Monte Carlo Simulation of Value at Risk (VaR) in Excel

Level 1 Chartered Financial Analyst (CFA ®): Sampling and Estimation