Home

Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

Bionic Turtle

Oct 16, 2019

11,755 views

Rank Correlations: Spearman's and Kendall's Tau (FRM T5-06)

Lognormal value at risk (VaR, FRM T5-01)

Fixed income: Bond DV01 (aka, price value of basis point, FRM T4-32)

Risk-neutral probabilities (FRM T5-07)

Value at Risk (VaR) Backtest (FRM T5-04)

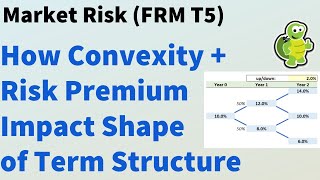

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

2015 - FRM : VAR Methods Part I (of 2)

Three approaches to value at risk (VaR) and volatility (FRM T4-1)

Value-at-risk (VaR) - variance-covariance and historical simulation methods (Excel) (SUB)

Fixed Income: Key rate shift technique (FRM T4-43)

Why par yields are the best interest rate measure

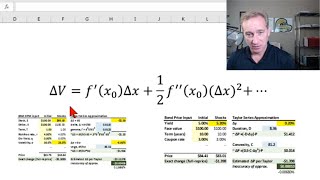

Delta-gamma value at risk (VaR) with the Taylor Series Approximation (FRM T4-4)

FRM: Lognormal value at risk (VaR)

Historical simulation (HS VaR): Basic and age-weighted (FRM T4-2)

Expected shortfall (ES, FRM T5-02)

Fed Chair Powell was trying to make sure the stock market didn't get disappointed: Komal Sri-Kumar

Coherent risk measures and why VaR is not coherent (FRM T4-5)

Mad Money - 09/20/24 | Audio Only

R Programming: Introduction: ggplot for capital market line (CML, R Intro-08)

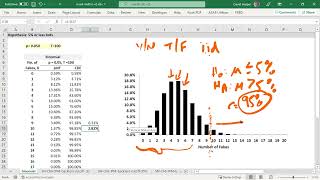

Binomial test: if Elon Musk samples 100 twitter accounts, how many bots (fakes) are too many?