Home

Fixed Income: Simple bond illustrating all three durations (effective, mod, Mac) (FRM T4-36)

Bionic Turtle

5 มิ.ย. 2019

การดู 17,160 ครั้ง

Fixed income: Effective Convexity (FRM T4-37)

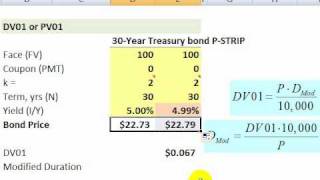

Fixed income: Bond DV01 (aka, price value of basis point, FRM T4-32)

CFA/FRM - Key Rate Duration

Interest Rate Risk and Return (2024 CFA® Level I Exam – Fixed Income – Learning Module 10)

Fixed Income Markets Explained┃Negative-Yielding Bonds, Duration & Yield Curves

Why par yields are the best interest rate measure

Fixed Income: Bullet versus Barbell Bond Portfolio (FRM T4-40)

Fixed Income Bond Valuations Prices and Yields (2024 CFA® Level I Exam – Fixed Income – LM 6)

Fixed Income: Key rate shift technique (FRM T4-43)

Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

Bond Duration and Bond Convexity Explained

Calculating Macauley, Modified, and Effective Bond Durations in Excel

Yield-Based Bond Convexity and Portfolio Properties (2024 CFA® Level I Exam – Fixed Income – LM 12)

Properties of Interest Rates (FRM Part 1 2023 – Book 3 – Chapter 16)

Fixed Income: Duration and Convexity Summary (FRM T4-42)

CFA level I: Fixed Income - Super Simplyfied Modified Duration Explained

Key Rate Duration & Key Rate Shifts Explained

Bond DV01 and duration

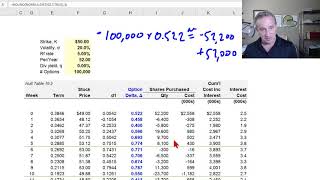

Dynamic option delta hedge (FRM T4-14)

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk