Home

Calculating Macauley, Modified, and Effective Bond Durations in Excel

Ryan O'Connell, CFA, FRM

21 ส.ค. 2023

การดู 8,397 ครั้ง

Key Rate Duration & Key Rate Shifts Explained

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

Bond Duration and Bond Convexity Explained

Using the Duration and MDuration functions in Excel

CFA/FRM - Key Rate Duration

What is modified duration? | Dejargoned

Bond Duration Explained Simply In 5 Minutes

สอนพื้นฐาน Excel ตั้งแต่เริ่มต้น แบบครบจบในคลิปเดียว!!

Black Scholes Option Pricing Model Explained In Excel

Modified Duration

What is the CFA? All You Need to Know w/ @straighttalks-ajsrmek323

Bond convexity

Portfolio Optimization in Excel: Step by Step Tutorial

Yield-Based Bond Convexity and Portfolio Properties (2024 CFA® Level I Exam – Fixed Income – LM 12)

Convexity of Bond

สอน Excel พื้นฐาน เบื้องต้น สำหรับผู้ที่เริ่มต้น ดูจบทำงานได้เลย | Excel by 9Expert

Fixed Income: Simple bond illustrating all three durations (effective, mod, Mac) (FRM T4-36)

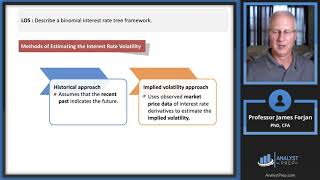

The Arbitrage-Free Valuation Framework (2024 Level II CFA® Exam – Fixed Income –Module 2)

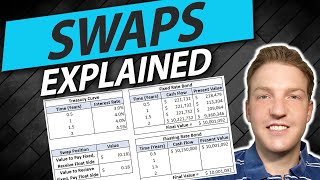

Interest Rate Swaps Explained | Example Calculation

สอน Excel ฟังก์ชัน VLOOKUP กับ MATCH สำหรับผู้เริ่มต้น ครบ พร้อมไฟล์ดาวน์โหลด ep.2