Home

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

Ryan O'Connell, CFA, FRM

Sep 18, 2023

11,793 views

Key Rate Duration & Key Rate Shifts Explained

Bond Duration and Bond Convexity Explained

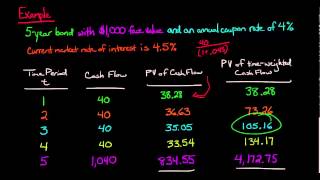

Bond Valuation: Interest Rate Risk, Price Risk and Reinvestment Risk

Calculating Macauley, Modified, and Effective Bond Durations in Excel

Efficient Frontier Explained in Excel: Plotting a 3-Security Portfolio

Bond convexity

Convexity of Bond

Interest Rate Swaps Explained | Example Calculation

Fixed Income: Simple bond illustrating all three durations (effective, mod, Mac) (FRM T4-36)

Macaulay Duration

Yield-Based Bond Convexity and Portfolio Properties (2024/25 CFA® Ll I Exam – Fixed Income – LM 12)

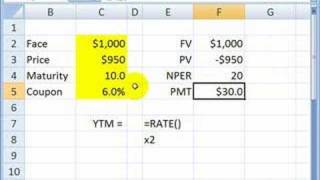

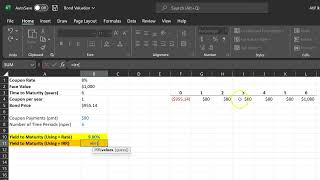

FRM: How to get yield to maturity (YTM) with Excel & TI BA II+

Calculate The Macaulay Duration Of A Bond In Excel

How to Calculate Yield To Maturity of a Bond -What is YTM and How to Use the Approximation Formula

Duration and convexity explained: bond interest rate sensitivity (Excel)

Coupon Rate vs Current Yield vs Yield to Maturity (YTM) | Explained with Example

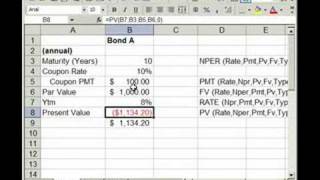

How to Calculate a Bond's Yield to Maturity (Using Excel)

Bond Pricing, Valuation, Formulas, and Functions in Excel

The Term Structure of Interest Rates Spot, Par, and Forward Curves (2024/2025 CFA® Ll I Exam – FI 9)

Probability of Default (PD) and Loss Given Default (LGD) Explained