Home

Bond Duration and Bond Convexity Explained

Ryan O'Connell, CFA, FRM

Mar 6, 2022

107,016 views

Calculating Macauley, Modified, and Effective Bond Durations in Excel

Bond Duration Explained Simply In 5 Minutes

CFA Level I Fixed Income - Approximate Modified Duration and Convexity Adjustment

Why Bond Yields Are a Key Economic Barometer | WSJ

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

FRM: You will never be scared of SWAPS after watching this!

How Fed Rate Cuts Affect The Global Economy

Killik Explains: Duration - The word every bond investor should understand

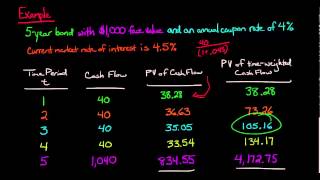

Macaulay Duration

CFA Level 1 Full Course: Yield-Based Bond Convexity and Portfolio Properties

BlackRock: The Conspiracies You Don’t Know

CFA level I: Fixed Income - Super Simplyfied Modified Duration Explained

What is Yield to Maturity? | How to Calculate YTM? | CA Rachana Ranade

Bond convexity

What is the Yield Curve, and Why is it Flattening?

Fixed Income Markets Explained┃Negative-Yielding Bonds, Duration & Yield Curves

Riding the Yield Curve and Rolling Down the Yield Curve Explained

Powell Explains Why the Fed Cut Rates by 50 Basis Points

CFA Level 1 Full Course: Yield-Based Bond Duration Measures and Properties

Yield-Based Bond Convexity and Portfolio Properties (2024/25 CFA® Ll I Exam – Fixed Income – LM 12)