Home

Bond Convexity and Duration | Convexity explained with example | FIN-Ed

FIN-Ed

Apr 14, 2019

55,120 views

Bond Duration and Bond Convexity Explained

Killik Explains: Duration - The word every bond investor should understand

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

Convexity

Bond convexity

ไอโฟน 16

Applying Duration, Convexity, and DV01 (FRM Part 1 2023 – Book 4 – Chapter 12)

MIT Has Predicted that Society Will Collapse in 2040 | Economics Explained

Convexity of Bond

How The Yield Curve Predicted Every Recession For The Past 50 Years

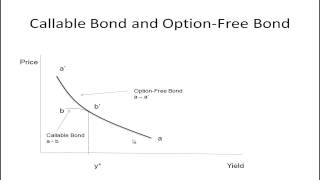

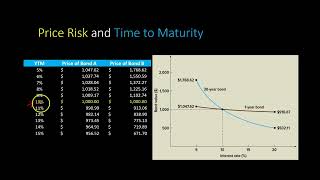

Bond Valuation: Interest Rate Risk, Price Risk and Reinvestment Risk

Yield-Based Bond Convexity and Portfolio Properties (2024/25 CFA® Ll I Exam – Fixed Income – LM 12)

Calculating Macauley, Modified, and Effective Bond Durations in Excel

CFA Level I- 2015 -Fixed Income : Risk and Return Part I(of 4)

Convexity

CFA Level 3 | Fixed Income: Macaulay Duration, Dispersion and Convexity

Fixed Income: Duration plus convexity to approximate bond price change (FRM T4-38)

Bond Portfolio Immunization

Bond Duration And Convexity Concept & Question (Nov 20 Exam / May 23 RTP)

CFA Level I Fixed Income - Approximate Modified Duration and Convexity Adjustment